- Update Report

- 11-Oct-2014

-

ProsperoTree.com first recommended ISGEC Heavy Engineering at Rs. 950 - Rs. 1050. The first research report can be accessed here (ISGEC Heavy Engineering Research Report). Since then ISGEC has performed very well and reached Rs. 3200 mark, making it a 3.2x (220% Returns) in less than a year.

Recently, ISGEC Heavy has announced its Q2FY15 results. In our understanding, the quarterly result is very good and further builds our conviction to HOLD ISGEC at current market cap of Rs. 2,350 crores.

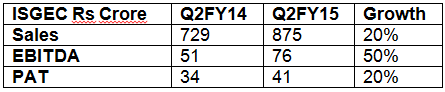

A. ISGEC Results Summary: The sales for ISGEC grew by 20% y-o-y and EBITDA grew by 50% y-o-y.

- The good results should be seen in light of Rs. 4,000 crores order book that ISGEC enjoyed at the start of this year. It seems that a large part of that order book has got executed in the current quarter.

- Based on the current quarter, there has been a healthy increase in the margin profile for ISGEC which has led to an EBITDA growth of 50% Y-o-Y. Though it is too early to comment on the margins profile of the future order book, we remain optimistic about the same.

B. Near Term Expectation: For the half-year ended September 2014, the company reported standalone sales of Rs. 1,577 and a profit of Rs. 66 crores. We think that for the full year, ISGEC is set to achieve a profit of Rs. 110-115 crores on a standalone basis. Add to this, the profits coming from subsidiaries as below:

- Saraswati Sugar Mill: In FY14 (6 months year), this business did not contribute any profits to the company. As the Sugar prices have remained subdued in most part of this year too, we do not expect any profits accruing to ISGEC from this subsidiary.

- ISGEC Hitachi Zosen JV: In this year, we expect ISGEC Hitachi Zosen JV to post a profit after minority interest of Rs. 10 crores.

With all this, ISGEC should be able to do a minimum profit of Rs. 125 crores and an EPS of Rs. 160-165. This indicates at CMP of Rs. 3,200, ISGEC is trading at 20x its current year earnings as against that of Thermax at 35x-40x.

C. Additional thoughts on ISGEC Story: For a capital good company like ISGEC, it is very difficult to gain any insights from one quarterly result. As we are fairly convinced that ISGEC is run by a very able management that is aggressive, focuses on quality and has a very clean balance sheet, it is better to focus on how the macro story that is shaping out. Below are some themes that can play out very well for ISGEC over the next 3-5 years period.

- Exports Business Opportunity: ISGEC has been able to increase its exports contribution from less than 20% a couple of years back to around 35-40% in FY13/FY14. ISGEC has a very strong name and near leader status, in Sugar Machineries segment across the world. The company has also been able to make inroads into a lot of geographies in the power boilers segments as well. Putting a number to the opportunity size is very difficult; however, it is easy to understand that opportunity for a player like ISGEC is fairly large as it is preparing for these opportunities for last 3 years. To put things under perspective, Thermax in a recent management interaction mentioned that Africa could well turn out to be a large opportunity. In Africa, ISGEC has already secured large orders in the Sugar Machineries space as well as Power Boilers space.

- Potential from Domestic markets: The fruits of the debottlenecking task taken by the new government will start to show up anytime in the next 1-2 years. The uptick in the domestic capex cycle may help ISGEC to garner order from small and mid-sized power plants (captive and otherwise). In addition to this, ISGEC is also planning to rope in a technology partner for large boilers used by UMPP that will help ISGEC to bid for larger projects. All in all, the opportunities from domestic market revival are quite big.

- ISGEC Hitachi Zosen JV: This Joint Venture between ISGEC and Hitachi Zosen was established in 2012 with a motive to cater to critical Process Equipment requirements of refineries, fertilizer & petrochemical industries, across the world. The technical & engineering skills of Hitachi Zosen and manufacturing expertise of ISGEC are intended to bring very healthy profits to this Joint Venture. This JV is operated out of the manufacturing facility of ISGEC in Dahej (Gujarat). The JV is now ready with an expanded capacity backed by strong order book of around Rs. 500 crores. This JV is looking to book orders for Gas-to-Liquid pressure vessels for all the emerging countries like India, China, Russia and South America.

D. Key Risks

- Overall depressed economic environment across India and major developing economies

- ISGEC is currently exposed to currency risk - exports constitute a large portion of its revenues. However, the margins are already at a cyclical low and can be easily improved if the domestic demand picks up.

E. Summary

To summarize, ISGEC is well positioned to ride the domestic capex revival as well as international demand. Its capable management and the thrust to continuously improve its competencies in the heavy engineering area should enable it to bag large orders and thereby gives visibility for 3-5 years period.

We recommend a HOLD on ISGEC Heavy at CMP of Rs. 3200. New investors can also look to add this stock in the current range of Rs. 3200 - 3500. However, the risks at this price are higher than that at our first recommendation of Rs. 950 – 1050.