- Update Report

- 8-Dec-2015

-

We recommended to Buy MT Educare at Rs. 111 in July2015 (MT Educare: Teaching + Technology= Good Returns)

Recently MT Educare announced its results for Q1FY16. Here is an update on the same:

-

On a standalone level, fee income increased from Rs. 45 cr in Q1FY15 to Rs. 51 cr in Q1FY16, showing a strong growth of 13.6%. In spite of no growth in student enrollment, the fee growth was led by reductions in discount offering. In the past, the discounts increased from 7.4% in FY12 to 13.1% of FY15. However, we expect the discounts to stabilize or decrease here on.

-

On the consolidated level, fees income increased from Rs 52 cr in Q1FY15 to Rs. 64 cr in Q1FY16, indicating 22% growth. This was mainly driven by strong enrollment in IIT coaching subsidiary Lakshya Educare Pvt Ltd (Lakshya Mumbai). The number of students increased from 640 in FY15 to around 1000 in FY16. The average fee per student for this course is around Rs. 2 lakh.

-

Consolidated other operating income increased sharply from Rs. 2 cr in Q1FY15 to Rs. 11 cr in Q1FY16. This was led by increased Government orders under Skill Development and increase of Robomate sales to non-MT students.

-

Other income stood at Rs. 2.1 crores in Q1FY16, up by 73% YoY on back of interest income received from Sri Gayatri Education Trust. The interest income will continue at the current level in future.

-

On the consolidated levels, Direct expense increased by 44% YoY mainly due to purchase of tablets / SD cards which are issued to students as a part of study materials. These tablets / SD cards are issued to MTEL students with pre-recorded lectures by the teachers.

-

Other expenses increased by 31% on a YoY basis as the advertisement spend increased substantially in Q1FY16 when compared to Q1FY15. We believe company will incur higher advertisement costs in FY16 as against Rs. 15 cr spent in FY15.

-

In spite of sale of its Mangalore University, Depreciation for the quarter increased to Rs. 3.5 cr. This is due to capitalization of intangible assets (mainly content generation) for its learning solution Robomate. It is important to note that in Q1FY15, there was a writeback of Rs. 5.5 cr for one-time reduction in depreciation due to change in depreciation policy that made changes in useful life of assets.

-

Finance cost for MTEL came to Rs. 0.3 cr due repayment of long term loans out of the sale proceeds of Mangalore PU college.

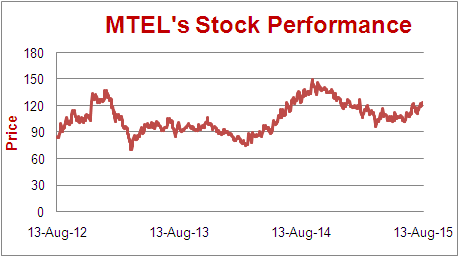

Conclusion: The result is in line with our expectation. We believe that the performance of the company will further improve because of reduction in discounts, enrollment growth in Lakshya and use of technology like Robomate and Learning Management System which will improve the student’s performance and experience. We remain optimistic on MTEL at CMP of Rs. 125 and maintain a Buy on MT Educare.

Dhruvesh Sanghvi is a Research Analyst registered with SEBI having registration No: INH000000875.

Definitions of Rating system:

- Fresh Recommendation Reports: These reports are first-time initiation reports on the concerned stock. Usually these reports are followed by updates on the same.

- Update Reports: These reports include result update, event updates, annual report analysis and/or any other information that may be useful for the investor in relation to the concerned stock. Most of these update reports will have our current view on the same.

- Buy: This means buying the concerned stock at current market price.

- Buy on Dips: This means buying the concerned stock on the explained fall in price.

- Hold: This means holding the concerned stock until further update.

- Sell Partial: This means selling half of the existing position in the concerned stock.

- Exit: This means completely exiting the concerned stock.

4. Explanation of Indicative Target Price: Achievement of Target Price does not imply Exit / Sell Partial. We will explicitly release Exit/ Sell Partial Report at an appropriate time. If required, Indicative Target Price could be revised based upon business performance, market environment or any other important event.

DISCLOSURES by RESEARCH ANALYST UNDER SEBI (RESEARCH ANALYSTS) REGULATIONS, 2014 is as under:

• Introduction: Prospero Tree Financial Services is an independent equity research proprietorship firm of Mr Dhruvesh Sanghvi.

• Business Activity: Prospero Tree Financial Services is committed in providing honest views, opinions and recommendations on financial markets opportunities.

• Report Written by: Dhruvesh Sanghvi

• Disciplinary History: None

• Terms & Conditions: https://www.prosperotree.com/termsofuse

• Details of Associates: Not Applicable

• Disclosure with regards to ownership and Material Conflicts of Interest:

1. Neither Dhruvesh Sanghvi, Prospero Tree Financial Services, its associates, its Research analysts hold any position in the subject company.

2. Neither Dhruvesh Sanghvi, Prospero Tree Financial Services, its associates, Research Analysts, nor its relatives, have more than 1% ownership of the subject company at the end of the month immediately preceding the date of publication of this report.

3. Neither Dhruvesh Sanghvi, Prospero Tree Financial Services, its associates, Research Analyst nor its relatives, has any other material conflict of interest at the time of publication of the research report or at the time of public appearance.

• Disclosure with regards to Receipt of Compensation:

1. Neither Dhruvesh Sanghvi, Prospero Tree Financial Services or its associates, or Research Analyst has received any compensation or other benefits from the subject company or the third party in connection with the research report in past twelve months.

2. Neither Dhruvesh Sanghvi, Prospero Tree Financial Services or its associates, or Research Analyst have managed or co-managed public offering or securities for the subject company in past twelve months.

• Other Disclosures:

1. The Research Analyst has not served as an officer, director, or employee of the subject company.

2. The Research Analyst is not engaged in market making activity for the subject company.